Macroeconomic Performance

Table 1: Overview of some macroeconomic indicators

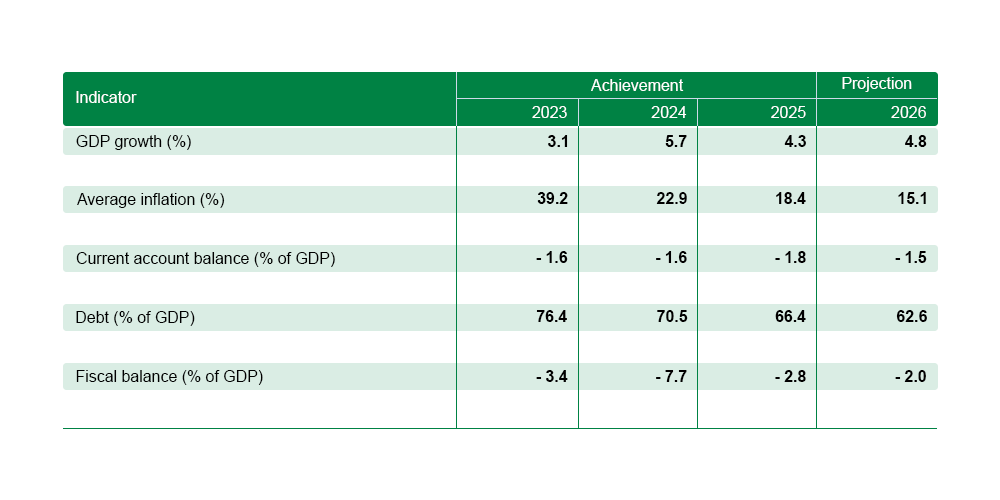

Ghana’s economic growth in 2023 surpassed expectations, growing by 2.9 per cent, compared to 3.8 per cent in 2022. This growth performance was facilitated by decent outputs in the agriculture and services sectors, while the industry sector capped overall growth with lower energy sector production. Average inflation accelerated to 37.5 per cent due to high energy and food prices and the impacts of a depreciating local currency. Fiscal consolidation remained broadly on course, as fiscal balance improved to -4.6 per cent of GDP in 2023 from -11.8 per cent of GDP in 2022. Public debt declined markedly from 93.3 per cent of GDP to 86.1 per cent of GDP as the authorities concluded the Domestic Debt Exchange Programme, which saw some holders of local government bonds accept a ‘haircut’ to ease the public debt burden. Current account balance also improved to -1.7 per cent of GDP in 2023 from -2.1 per cent of GDP in 2022.

Outlook

The economy is projected to grow by 3.1 per cent in 2024 and 3.5 per cent in 2025 as the economy continues on a path to recovery. The growth projections have been capped by the effects of the cedi depreciation, high energy prices and the epileptic electricity supply the country has experienced in 2024. Average inflation is projected to decline to 25.5 per cent in 2024 and further to 23.5 per cent in 2025. Fiscal balance is projected to worsen to -5.0 per cent of GDP, predicated on a possible miss of the revenue target, given the suspension of the VAT on electricity sales. Furthermore, given that it is an election year, which is expected to be keenly contested, expenditure controls are not likely to be very effective in 2024. Fiscal balance will improve to -4.3 per cent of GDP in 2025. The debt-to-GDP ratio is projected to decline to 83.6 per cent of GDP under the assumption that the government will reach an agreement with its external creditors on the treatment of bilateral debt. Public debt is projected to decline further to 80.9 per cent of GDP in 2025. The current account balance is projected to increase slightly to -1.9 per cent of GDP in 2024 on account of election-related imports while increasing further to -2.1 per cent of GDP in 2025.

Probable Headwinds

Ghana’s economy is still exposed to exchange rate and inflationary pressures. The elections of 2024 pose severe risks to fiscal consolidation, while the electricity supply shortfalls could cap economic growth. Agriculture output, including the cocoa sector, could suffer from insufficient rainfall, which will have implications for food security and export proceeds.